We'll introduce e-invoices step-by-step to make the change easy. We've planned how to do it, considering how much money businesses make, so everyone has enough time to prepare and get used to e-invoices.

⚠️ Micro-businesses earning below RM150,000 are exempted, but voluntary adoption is encouraged.

According to LHDN, all businesses in Malaysia will have to use e-invoices soon. But what does "taxpayer" mean?

In Malaysia, a taxpayer is someone or a group that earns money and must pay taxes to the government. These taxes help the government run the country by funding services like roads, healthcare, and schools.

According to the Income Tax Act 1967, a taxpayer can be anyone or any organization that has to pay income tax in Malaysia. This includes individuals, companies, and other groups that make money in the country.

So, taxpayers are basically anyone or any organization that earns taxable income in Malaysia. Almost everyone or every entity, except for some exceptions, will have to use e-invoices, according to the e-invoicing guide.

Generating e-invoices in Malaysia follows similar steps, with minor variations based on your chosen method (API or Portal) and transaction type (B2B or B2C).

Taxpayers can pick how they want to send e-invoices to LHDN based on their situation and what they need for their business. This makes switching to e-invoices easier.

Taxpayers have two options for sending electronic invoices:

Using e-invoicing helps businesses in many ways

E-Invoicing speeds up billing and payment cycles by sending invoices instantly. No more waiting for mail or manual processing—just quick, direct transactions.

Invoices are automatically reported to LHDN as soon as they’re issued, keeping your business in line with tax rules without extra effort.

No printing, no postage, and no physical storage means less spending on office supplies and admin time.

Digital invoicing uses secure, trackable systems that reduce the chance of invoice tampering, duplicates, or fake claims.

Going digital cuts down on paper usage, helping your business reduce waste and support sustainability efforts.

🟢 Government grants & tax deductions of up to RM50,000 (2024-2027) available for MSMEs implementing e-Invoicing.

What is Interim Relaxation Period? It is a 6-month grace period after each phase’s implementation date where enforcement is more lenient, designed to help businesses adapt without penalties for minor non-compliance.

E-invoicing uses the same patterns and rules for invoices, making sure they all look and say the same things. This helps them move easily between different computer systems.

Simple format easy for people and computers to read. More people using it for e-invoices because it's easy and works well with different systems.

A flexible way to describe information in a format that's easy for people to read. Many people use it for e-invoices because it's flexible and easy to understand.

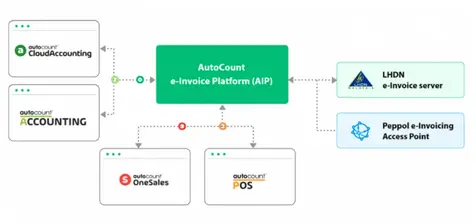

E-invoicing in AutoCount POS, Autocount Accounting, AutoCount Cloud Accounting, and AutoCount Onesales is facilitated by the AutoCount E-Invoice Platform (AIP). This platform automatically sends every invoice to the LHDN MyINVOIS portal. We developed the AIP to simplify e-invoice submissions to the LHDN MyINVOIS portal. If you have a large number of invoices to submit, let the AIP handle it to save time compared to manual submission.

Our AutoCount E-Invoice Solution automates the generation and submission of consolidated and self-billed e-invoices directly from the AutoCount E-Invoice Solution. In case the LHDN MyINVOIS server experiences downtime, the Autocount E-Invoice Portal (AIP) will keep trying to submit all e-invoices to LHDN until they are successfully processed. This solution streamlines the invoice submission process to LHDN without manual intervention, making it fully automated.

No, the LHDN e-Invoice applies to both domestic and international transactions, including imports and exports.

Yes, e-Invoicing will be mandatory for all businesses, following a phased implementation based on their annual turnover or revenue threshold.

Yes, all industries must comply. However, specific income types and transactions may be exempt, as outlined in Section 1.6 of the LHDN e-Invoice Guideline.

Yes, but once the revenue exceeds the threshold, the exemption no longer applies.

No, once verified, it cannot be edited. You must cancel it within 72 hours or issue an adjustment (debit/credit/refund note) afterward.

Suppliers have a 72-hour window to cancel a verified e-Invoice.

After 72 hours, use a debit note, credit note, or refund note to make adjustments. There is no specific timeframe for this; follow your company policy.

Yes, buyers can reject an e-Invoice within 72 hours of issuance.

You must obtain the buyer’s details. If the foreign buyer has no TIN, use the placeholder “EI00000000020” as per Section 10.5 of the Specific Guideline.

Yes, e-Invoices can be issued in any currency. The RM-equivalent is optional.

Yes, a refund note e-Invoice is required unless the refund is due to an overpayment, payment made in error, or return of a security deposit.

It depends on the context. Refer to Section 5 of the Specific Guideline for case-specific requirements.

Yes, draft or proforma invoices can be created, but only validated e-Invoices are accepted for tax purposes.

IRBM validates e-Invoices to ensure they conform to the required format and data structure, as described in Section 2.4.3 of the guideline.

Malaysia adopts the Continuous Transaction Control (CTC) model, where validation occurs in near real-time by IRBM.

Yes, a Software Development Kit (SDK) will be provided to assist with integration.

Thresholds are based on the annual turnover or revenue reported in FY22 Audited Financial Statements.

Yes, IRBM is conducting engagement sessions with stakeholders to provide updates and gather feedback on the e-Invoice implementation.

You can email your queries to myinvois@hasil.gov.my.

Businesses should review the official LHDN guidelines, assess their current invoicing systems, attend IRBM engagement sessions, and begin system integration or updates to ensure compliance before their mandated implementation date.