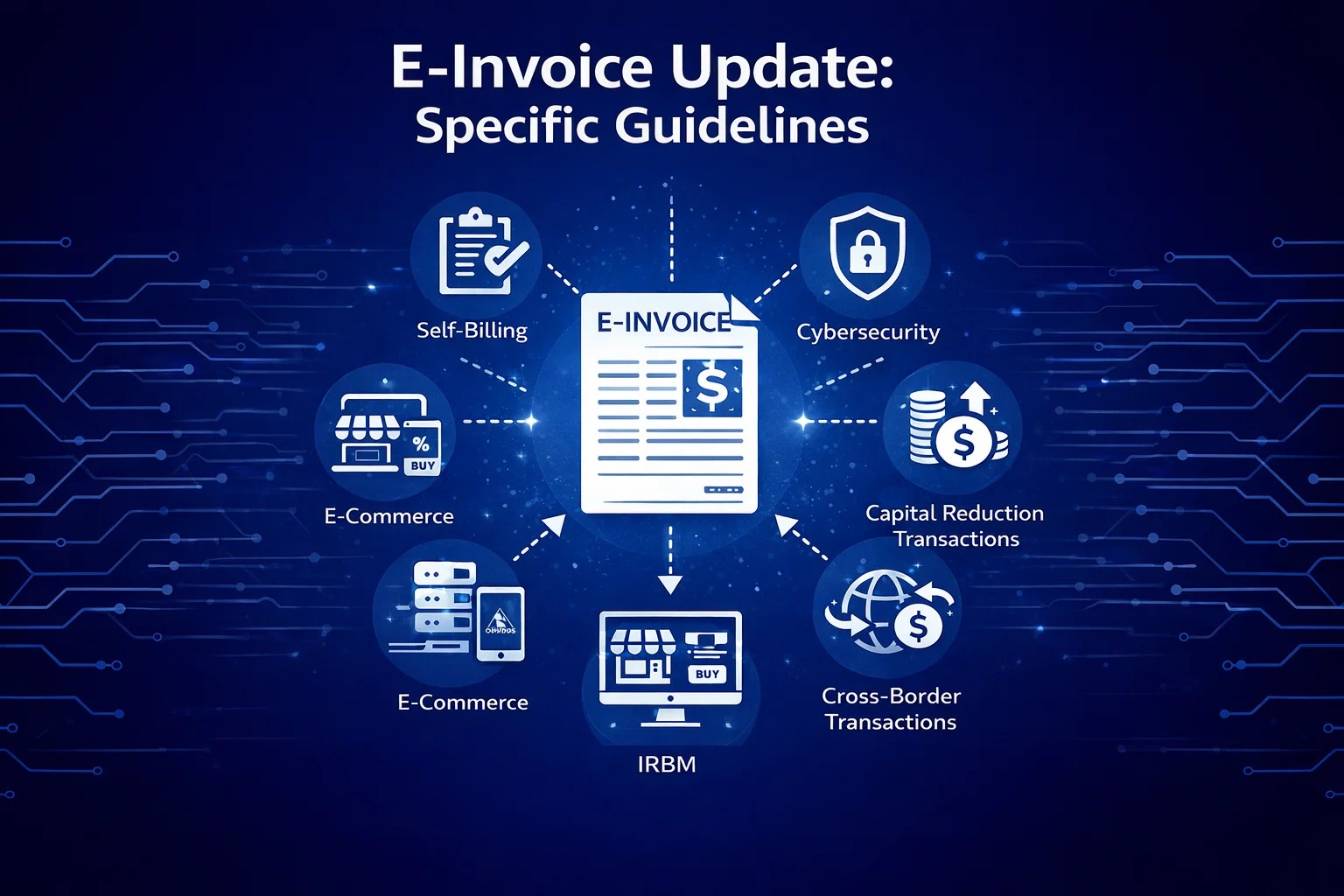

E-Invoice Update: Specific Guidelines – January 28th, 2025

The Inland Revenue Board of Malaysia (IRBM) has released Version 4.0 of the e-Invoice Specific Guideline on January 28, 2025. This updated version introduces new clarifications and additions to improve compliance with e-Invoicing in Malaysia, including guidelines for self-billing, cross-border transactions, and e-commerce businesses. It also highlights key changes regarding interest payments, capital reduction transactions, and cybersecurity measures. Stay updated with the latest requirements to ensure smooth e-Invoice implementation for your business.

Introduction

The Inland Revenue Board of Malaysia (IRBM) has released Version 4.0 of the e-Invoice Specific Guideline on January 28, 2025. This guideline provides detailed explanations and clarifications on the implementation of e-Invoicing in Malaysia.

Update Detail

| No | Paragraph in eInvoice Specific Guideline | Before (Version 3.1) | After (Version 4.0) |

|---|---|---|---|

| 1. | 3.6.5 | None |

(a) transactions with individuals (who are not conducting a business) (b) interest payment to public at large (regardless businesses or individuals) (c) claim, compensation or benefit payments from the insurance business of an insurer to individuals (who are not conducting a business), government, government or state authority, government authority, state (d) self-billed circumstances involving taxpayers’ overseas branches or offices |

| 2. | 8.3 | None |

For e-Invoice purposes, Buyer shall issue self-billed e-Invoices for the following transactions: (a) Payment to agents, dealers, distributors, etc. (refer to Section 9 of this e-Invoice Specific Guideline for further details) (b) Goods sold or services rendered by foreign suppliers (refer to Section 10.4 of this e-Invoice Specific Guideline for further details) (c) Profit distribution (e.g., dividend distribution) (refer to Section 11 of this e-Invoice Specific Guideline for further details) (d) Electronic commerce (“e-commerce”) transactions (refer to Section 14 of this e-Invoice Specific Guideline for further details) (e) Pay-out to all betting and gaming winners (f) Transactions with individuals (who are not conducting a business) (applicable only if the other self-billed circumstances are not applicable) (g) Interest payment, except: – Businesses (e.g., financial institutions) that charge interest to public at large – Interest payment made by employee to employer – Interest payment made by foreign payor to Malaysian taxpayers – Interest payment to a related company providing centralised treasury services – Late payment interest or charges imposed by Malaysian taxpayers. Note: The Supplier is required to issue e-Invoice for exceptions mentioned above. (h) Claim, compensation or benefit payments from the insurance business of an insurer (i) Payment in relation to capital reduction, share / capital / unit redemption, share buyback, return of capital or liquidation proceeds. Note that the Buyer is required to issue self-billed e-Invoice in accordance with the following timing of issuance: If there is a written agreement: – If no approval is required from the government or state government, the date of issuance will be the date of the agreement. – If approval is required from the government or state government, the date of issuance will be the date of such approval, or if the approval is conditional, the date of issuance will be the date in which the last condition is satisfied. If there is no written agreement: Date of completion |

| 3. | EXAMPLE 16 | None |

Cee Sdn Bhd has obtained RM10 million loan for business purpose from its holding company, Beeny Sdn Bhd. Beeny Sdn Bhd charges an arm’s length interest to Cee Sdn Bhd. In line with Section 8.3(g) of this e-Invoice Specific Guideline, as Beeny Sdn Bhd is not an entity providing centralised treasury services to its group, Cee Sdn Bhd is required to assume the role of Supplier and issue self-billed e-Invoice for the interest paid to Beeny Sdn Bhd. |

| 4. | Example 17 – 20 | None |

Example 17: Cee Sdn Bhd now obtained the loan from Yee Sdn Bhd, a related company offering centralised treasury services. Yee Sdn Bhd must issue an e-Invoice to Cee Sdn Bhd. Example 18: Kayan Jaya Sdn Bhd imposes a late payment charge of 3% on overdue invoices. It must issue an e-Invoice for the interest received. Example 19: Kelip Karat Berhad provides a staff loan with 3% interest. It must issue an e-Invoice for the interest received. Example 20: Mark, as the estate administrator of John’s money-lending business, receives interest from Syarikat Deepak. Deepak must issue a self-billed e-Invoice for the interest paid. |

| 5. | Table 8.1 | None |

Transaction: Payment related to capital reduction, share/unit redemption, buyback, return of capital, or liquidation proceeds. Supplier: Investor Buyer: Investee |

| 6. | Appendix – Table 3 | None |

Transaction: Payment in relation to capital reduction, share/unit redemption, buyback, return of capital, or liquidation proceeds. Supplier: Investor Buyer: Investee |

| 7. | Appendix – Table 5 | None | Area/Industry: Financial Services, Stockbroking, and Unit Trust |

Link to FAQ: Financial Services FAQ

Key Updates in Version 4.0

This version replaces the previous Version 3.1 (issued on October 4, 2024) and includes several additions and clarifications to improve compliance and understanding.

New Clarifications and Additions

- Transactions with Buyers: More details on how businesses should handle e-Invoice issuance.

- Employment Benefits: Clarification on how employment-related perquisites should be invoiced.

- Self-Billed e-Invoice: New guidelines on parties involved in self-billing.

- Foreign Income: Updates on handling cross-border transactions.

- E-Commerce Transactions: Clearer rules for online businesses issuing e-Invoices.

- Cybersecurity Measures: Emphasis on securing e-Invoice data.

- Interim Relaxation Period: Special conditions for businesses transitioning to e-Invoicing.

For full details, visit the official IRBM website or refer to the latest e-Invoice Specific Guideline (Version 4.0).

Learn E-Invoicing with Our Expert-Led Classes

Ready to master e-invoicing and streamline your business? Join our comprehensive class and get hands-on guidance!