E-Invoice Implementation in Malaysia

Navigate Malaysia’s e-Invoice mandate with confidence. A complete guide to LHDN E-Invoice implementation timelines, MSME exemption criteria, and essential compliance tips based on annual turnover.

Introduction to E-Invoicing Malaysia

Malaysia is embarking on a significant digital transformation with the mandatory implementation of E-Invoicing. Specifically, this system is required by the Inland Revenue Board of Malaysia (LHDN), requires businesses to issue, transmit, and validate invoices through a standardized digital platform.

This comprehensive guide explains everything Malaysian businesses need to know about E-Invoice implementation, including phased timelines, MSME exemptions, technical requirements, and practical steps for compliance. In addition, whether you’re a large corporation or a small enterprise, understanding these changes is crucial for smooth operations and avoiding penalties.

E-Invoice Implementation Timeline

The implementation of e-Invoices will occur in phases, based on a company’s annual turnover. Therefore, the following is the official timeline for compliance:

| Implementation Date | Annual Revenue Threshold | Annual Revenue Threshold |

|---|---|---|

| 1 August 2024 | Exceeding RM100 million | Large enterprises |

| 1 January 2025 | RM25 million - RM100 million | Medium-large enterprises |

| 1 July 2025 | RM5 million - RM25 million | Medium enterprises |

| 1 January 2026 | RM1 million - RM5 million | Small enterprises |

| 1 July 2026 | Below RM1 million | Micro enterprises |

However, MSMEs with annual turnover below RM500,000 are exempt from the e-Invoice requirement. Despite this exemption, the government encourages voluntary adoption of the e-Invoice system.

Exemption Criteria for MSMEs: Three Key Scenarios

In general, businesses with an annual turnover below RM500,000 are exempted from the mandatory e-Invoice requirement. However, three scenarios exist where MSMEs are not exempted from issuing e-Invoices, even if their revenue is below the RM500,000 threshold.

-

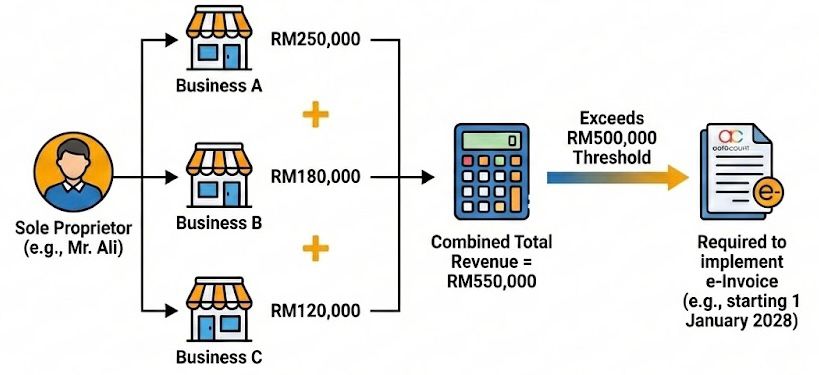

Scenario 1: Sole Proprietor with Combined Business Revenue Above RM500,000

For sole proprietors, if they run multiple businesses, the combined total revenue of all their businesses is considered when determining whether they are exempt. If the combined revenue exceeds RM500,000, they are required to implement e-Invoice, regardless of the revenue of individual businesses.

- Example

Mr. Ali operates three businesses:

- Business A: RM250,000

- Business B: RM180,000

- Business C: RM120,000

The total combined revenue of RM550,000 exceeds the RM500,000 threshold. Hence, Mr. Ali will be required to implement e-Invoice starting 1 January 2028, two years after surpassing the threshold.

-

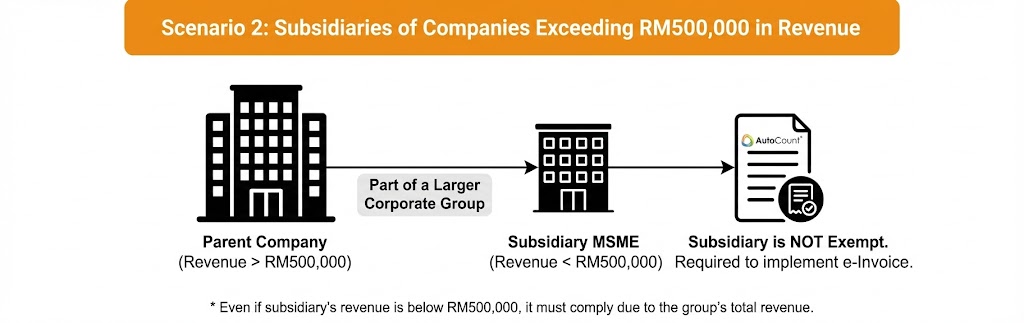

Scenario 2: Subsidiaries of Companies Exceeding RM500,000 in Revenue

If an MSME is a subsidiary of a company whose annual turnover exceeds RM500,000, the subsidiary is not exempted from the e-Invoice system. Even if the subsidiary’s revenue is below RM500,000, it must comply with the e-Invoice rules because it is part of a larger corporate group that is mandated to implement e-Invoice.

- Example

If an MSME is a subsidiary of a company whose annual turnover exceeds RM500,000, the subsidiary is not exempted from the e-Invoice system. Even if the subsidiary’s revenue is below RM500,000, it must comply with the e-Invoice rules because it is part of a larger corporate group that is mandated to implement e-Invoice.

-

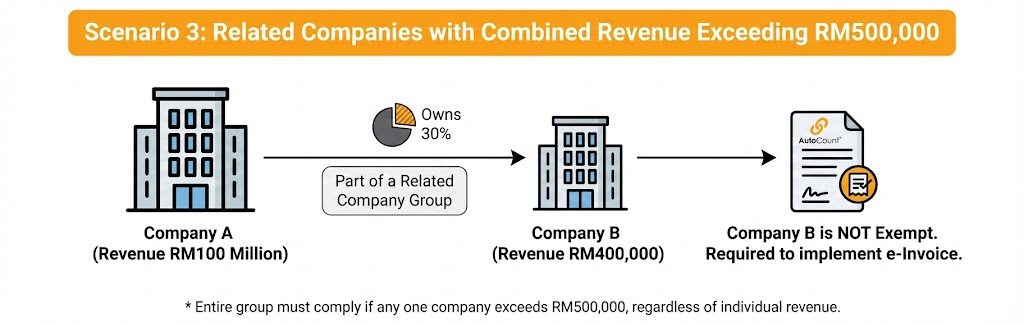

Scenario 3: Related Companies with Combined Revenue Exceeding RM500,000

If a company is part of a related company group, and any one of the related companies exceeds RM500,000 in revenue, the entire group must comply with the e-Invoice system. This applies regardless of the individual revenue of each company within the group.

- Example

- Company A owns 30% of Company B.

- Company A has an annual revenue of RM100 million and is required to implement e-Invoice.

- Even if Company B has revenue of RM400,000, it is still required to implement e-Invoice because it is part of the related company group of Company A.

Important Implementation Rules for MSMEs

-

Timeline for Newly Non-Exempt Businesses

MSMEs that exceed the RM500,000 threshold must implement e-Invoice from 1 January of the second year after they exceed the threshold.

- Example

Winner Fertilizer Sdn. Bhd. exceeded RM500,000 in revenue as of 31 August 2026. Therefore, they must begin issuing e-Invoices starting 1 January 2028.

-

No Re-Exemption Policy

Once a business has been mandated to implement e-Invoice, it cannot be exempted again, even if its annual turnover falls below RM500,000 in subsequent years.

- Example

Even if Winner Fertilizer Sdn. Bhd. has revenue of RM480,000 in 2027, it must still implement e-Invoice starting 1 January 2028.

Conclusion

Malaysia’s e-invoicing initiative represents a significant step toward digital modernization of business transactions. However, while the transition requires preparation and adaptation, the long-term benefits of increased efficiency, reduced costs, and improved compliance make it a valuable investment for Malaysian businesses.

Ultimately, by understanding the specific requirements, timelines, and exemption criteria outlined in this guide, businesses can navigate the implementation process smoothly and position themselves for success in Malaysia’s digital economy.

Frequently Asked Questions

Are MSMEs in Malaysia required to issue e-Invoice?

In general, businesses with an annual turnover below RM500,000 are exempted from the mandatory e-Invoice requirement. However, there are three specific scenarios where this exemption does not apply.

How will sole proprietorships be affected by e-Invoice implementation?

For sole proprietorships with more than one business, the combined revenue of all businesses registered under the same name is used to determine whether the RM500,000 threshold has been exceeded.

Can MSMEs be exempted again if their revenue falls below RM500,000?

No, once a business has been mandated to implement e-Invoice, it cannot be exempted again, even if its annual turnover falls below RM500,000 in subsequent years.

Is e-invoice mandatory for small businesses in Malaysia?

Yes. From 1 January 2026, all businesses—including MSMEs—must comply unless specifically exempted.

Learn E-Invoicing with Our Expert-Led Classes

Ready to master e-invoicing and streamline your business? Join our comprehensive class and get hands-on guidance!