Malaysia Minimum Wages 2024: RM1,700 Hike, PWP Incentives & Essential Payroll Compliance Roadmap

A clear guide summarising Malaysia’s RM1,700 minimum wage: who must comply, when it becomes mandatory (Feb 2025 and Aug 2025 phases), and what it means for payroll. Covers compliance obligations, wage breakdowns (monthly, daily, hourly) and implications for employers across sectors.

Introduction

The enforcement of the Minimum Wages Order 2024 (MWO 2024) marks a pivotal moment in Malaysia’s industrial relations landscape. This crucial legislation, which raises the statutory minimum wage to RM1,700 per month, is more than a simple cost adjustment; it is the foundation of the government’s dual strategy to elevate worker welfare and national productivity. For employers, particularly those managing payroll and compliance, mastering the nuances of the MWO 2024 is essential to avoid catastrophic penalties and strategically integrate with the voluntary Progressive Wage Policy (PWP). This detailed analysis provides the complete roadmap for full compliance.

1. MWO 2024: The Legal Mandate and RM1,700 Minimum Wage Floor

The new national minimum wage is officially mandated under the legal text P.U. (A) 376/2024, enforced through the National Wages Consultative Council Act 2011 (Act 732). This minimum wage adjustment—the sixth since 2011—underscores the government’s commitment to ensuring a dignified wage floor.

1.1 Decoding 'Basic Salary' (Gaji Pokok): The Definition of Minimum Wage (Critical Compliance Point)

A critical legal distinction under the MWO 2024 is that the minimum wage strictly refers ONLY to the basic salary (gaji pokok). This is perhaps the most misunderstood aspect of the minimum wage law:

- Included: Exclusively the basic salary component.

- Explicitly Excluded: Fixed allowances, variable incentives, commissions, overtime pay, or any other additional remuneration.

This explicit definition prevents the misuse of variable pay or existing allowances to artificially meet the new minimum wage standard. Businesses must ensure the contractual basic salary is RM1,700 or higher to achieve compliance.

For employers seeking deeper clarification on what counts as “wages” under Malaysian law, refer to our Definition of Wages under the Employment Act 1955 . It explains how basic pay, allowances, and deductions are interpreted in official compliance audits.

1.2 Case Study 1: Total Payout Does Not Equal Minimum Wage

Many organizations erroneously calculate the minimum wage by summing all cash components. This illustration proves why a high total payout fails to meet the legal definition if the basic salary is deficient.

| Component | Example 1 (Compliant) | Example 2 (Non-Compliant) | Example 3 (Non-Compliant) |

|---|---|---|---|

| Basic Salary | RM1,800 | RM1,500 | RM1,500 |

| Fixed Allowances | — | RM200 | RM800 |

| Commission | RM200 | RM300 | — |

| Overtime | — | — | RM200 |

| Total Payout | RM2,000 | RM2,000 | RM2,500 |

| Compliant with MWO 2024? | ✔ Yes | ❌ No | ❌ No |

Compliance Mandate: For minimum wage compliance, only the Basic Salary in Example 1, at RM1,800, is sufficient. Examples 2 and 3 are non-compliant, despite the high total payouts, because the basic salary is below the RM1,700 minimum wage.

1.3 Mandatory Conversion Rates: Daily and Hourly Minimum Wage Standards

To standardize pay for non-monthly earners and prevent disputes, the MWO 2024 dictates fixed statutory conversion rates:

| Monthly Wage (RM) | Work Days Per Week | Daily Rate (RM) | Hourly Rate (RM) |

|---|---|---|---|

| 1,700 | 6 Days | 65.38 | 8.72 |

| 1,700 | 5 Days | 78.46 | 8.72 |

| 1,700 | 4 Days | 98.08 | 8.72 |

The equivalent hourly minimum wage of RM8.72 per hour applies uniformly to all employees, including part-timers, across the nation.

The daily rate must be derived from the monthly basic wage using a 52-week year and the employee’s contractual workdays per week.

Statutory formula:

Minimum wage RM1,700/month → Daily rate:

- 6 days/week: RM 65.38

- 5 days/week: RM 78.46

- 4 days/week: RM 98.08

Hourly rate:

Hourly rate = (Rate of Monthly Minimum Wage × 12 Months) ÷ (52 weeks × Maximum Hours per Week)

- Base MWO 2024 is 45 hours/week → RM 8.72/hour

2. Hidden Payroll Pitfalls: Daily Wage Calculation Errors

A silent compliance killer is the incorrect calculation of the daily minimum wage using obsolete or generalized divisors, often resulting in either legal jeopardy (underpayment) or unnecessary business costs (overpayment).

2.1 Case Study 2: Underpayment Risk (Using Incorrect Divisors)

Many legacy payroll systems use approximated working days per month (e.g., 22 or 18) instead of the statutory formula. This common error results in a daily rate that is less than the legally mandated rate, risking immediate minimum wage underpayment and fines.

| Monthly Basic (RM) | Workdays/Week | Incorrect Daily Rate (Legacy Divisor) | Correct Daily Rate (Statutory) | Variance | Implication |

|---|---|---|---|---|---|

| 1,700 | 6 | (1,700 ÷ 26) = 65.38 | 65.38 | RM0.00 | — |

| 1,700 | 5 | (1,700 ÷ 22) = 77.27 | 78.46 | -RM1.19 | Potential Minimum Wage Underpayment (Penalty Risk) |

| 1,700 | 4 | (1,700 ÷ 18) = 94.44 | 98.08 | -RM3.64 | Potential Minimum Wage Underpayment (Penalty Risk) |

Action: Replace all legacy payroll divisors with the MWO 2024 statutory rates to mitigate underpayment risk under the minimum wage law.

Payroll accuracy doesn’t stop at daily wage computation. It also extends to how unpaid leave and mid-month salary adjustments are calculated. For a full breakdown of the correct formulas and statutory methods, read our Guide on Calculating Unpaid Leave and Partial Month Salary in Malaysia.

2.2 Case Study 3: Cost Leakage Risk (Overpayment by Approximation)

Conversely, some HR teams use divisors (e.g., 20 or 16) that, while ensuring compliance, inflate the actual daily rate beyond the minimum wage requirement, leading to significant, recurrent overpayments.

| Monthly Basic (RM) | Workdays/Week | Incorrect Daily Rate (Approximated Divisor) | Correct Daily Rate (Statutory) | Variance | Implication |

|---|---|---|---|---|---|

| 1,700 | 6 | (1,700 ÷ 26) = 65.38 | 65.38 | RM0.00 | — |

| 1,700 | 5 | (1,700 ÷ 20) = 85.00 | 78.46 | +RM6.54 | Potential Business Loss |

| 1,700 | 4 | (1,700 ÷ 16) = 106.25 | 98.08 | +RM8.17 | Potential Business Loss |

Cost Impact: A recurring daily variance, such as the RM6.54 overpayment shown above, quickly accrues, resulting in thousands of Ringgit in annual leakage across a moderate workforce. Standardize all daily wage calculations to the precise statutory figures.

3. Commission-Based Employees: The Zero-Basic Minimum Wage Risk

Sectors that traditionally use high variable pay (e.g., sales, logistics, F&B) face the highest compliance hazard under the MWO 2024 due to the strict definition of basic salary and the minimum wage floor for total earnings.

3.1 Scenario 4: The Car Dealership Sales Executive

A non-compliant model is structuring employment with “zero basic salary” or “low basic, high commission” only.

Minimum Wage Shortfall = Legal Minimum Wage – (Basic Salary + Commission/Bonus) = RM 1,700 – Total Payout

| Compensation Structure | Sales Executive A (RM) | Sales Executive B (RM) | Compliance Status |

|---|---|---|---|

| Basic Salary (Gaji Pokok) | RM 0.00 | RM 1,000.00 | Critical Risk |

| Commission / Bonus (Low Month) | RM 800.00 | RM 500.00 | — |

| Total Payout (Low Month) | RM 800.00 | RM 1,500.00 | — |

| Minimum Wage Shortfall | -RM 900.00 | -RM 200.00 | Non-Compliant |

The Legal Violation

Mandatory Basic Salary: An employee under a contract of service (like a sales executive) must have a contractual basic salary of at least RM1,700. A zero or insufficient basic salary is a direct legal violation.

Minimum Floor on Total Earnings: Even if a company is allowed to pay based on commission, the MWO 2024 mandates that the employee’s total monthly wages received must not be less than RM1,700.

- Executive A's RM800 total payout and Executive B's RM1,500 total payout in a low sales month are both immediate, severe violations of the minimum wage floor.

Consequence: These violations trigger KESUMA enforcement, leading to immediate fines of up to RM10,000 per affected employee under Act 732, plus compulsory payment of all wage arrears.

3.2 Scenario 5: Offsetting Basic Salary with Unlawful Deductions

Another common non-compliance method involves meeting the RM1,700 basic salary requirement on paper, but immediately neutralizing the increase through forced deductions.

| Compensation Structure | Employee C (RM) | Implication |

|---|---|---|

| Basic Salary (Gaji Pokok) | RM1,700 | Appears compliant |

| Compulsory Dormitory Fee Deduction | (RM300) | Requires DGL approval and consent |

| Mandatory Uniform/Equipment Fee Deduction | (RM100) | Highly regulated deduction |

| Net Payable Before Statutory Deductions | RM1,300 | De facto minimum wage underpayment |

The Employment Act 1955 heavily restricts deductions. Using compulsory deductions for fees like dormitories or equipment without the employee’s express written consent and, in many cases, prior approval from the Director General of Labour (DGL), is an illegal form of wage suppression. This practice will be treated as a failure to pay the statutory minimum wage.

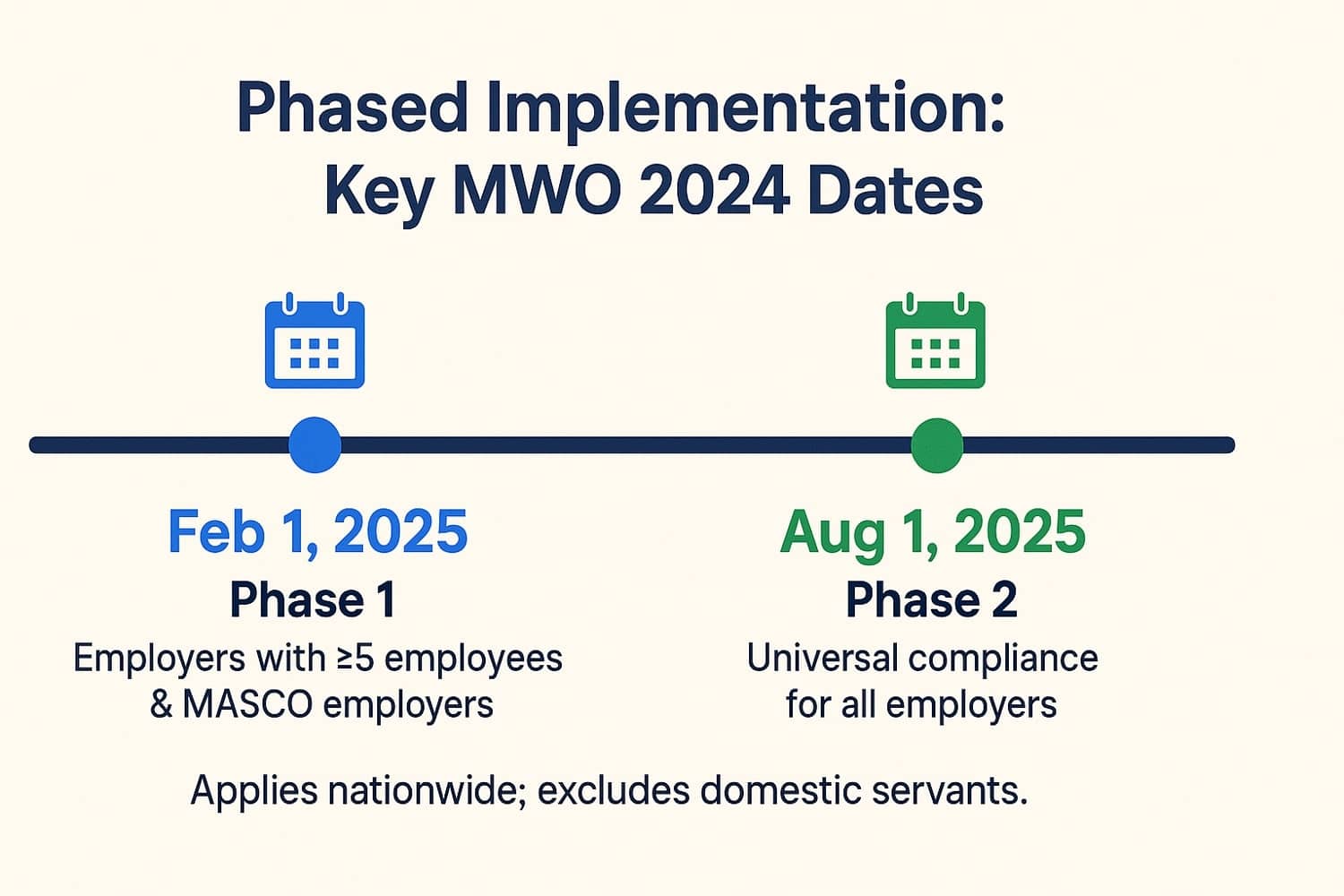

4. Phased Implementation: Key MWO 2024 Dates

The new minimum wage rollout follows a strict two-phase schedule:

4.1 Phase 1: Immediate Compliance (February 1, 2025)

The RM1,700 minimum wage is immediately mandatory for:

- Employers with five or more employees.

- MASCO Employers: All employers engaged in professional activities under the Malaysia Standard Classification of Occupations 2020, irrespective of their headcount.

4.2 Phase 2: Universal Compliance (August 1, 2025)

The six-month deferment period ends on July 31, 2025. From August 1, 2025, the RM1,700 minimum wage becomes fully applicable to ALL employers nationwide, without exception.

4.3 Who is Covered?

The minimum wage applies across all regions (Peninsular Malaysia, Sabah, and Sarawak) and covers all private sector employees, including foreign workers and contract apprentices. The only explicit exclusion is domestic servants (pekhidmat domestik).

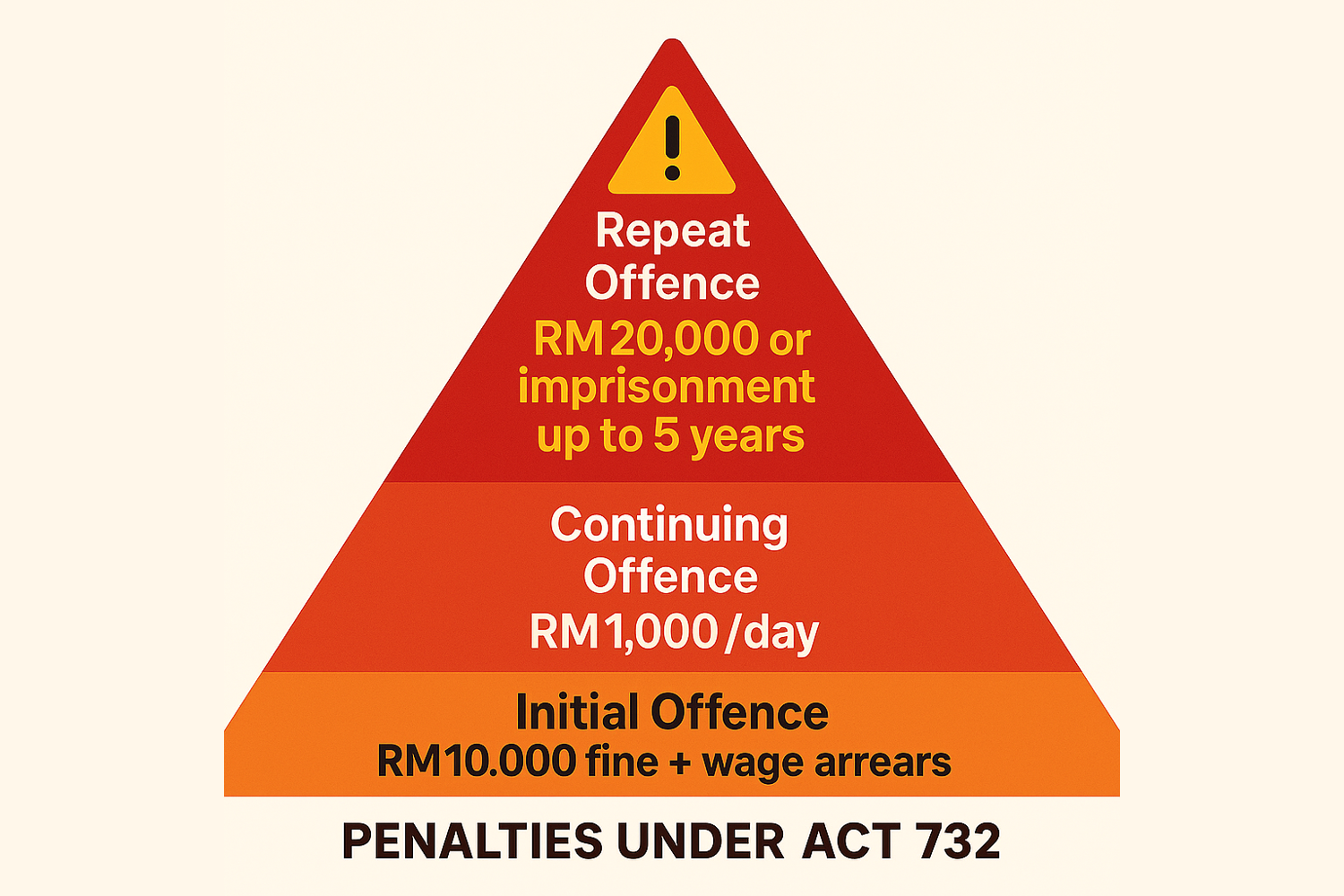

5. The High Cost of Non-Compliance: Penalties Under Act 732

Failure to comply with the MWO 2024 is an offence under Act 732. KESUMA is actively enforcing this law, and the penalties are structured to ensure that the cost of non-compliance far outweighs the cost of adopting the new minimum wage.

5.1 Fine Structure: Up to RM10,000 Per Employee

The most potent deterrent is the per-employee penalty structure:

- Initial Offence (Section 43): A fine of up to RM10,000 for EACH affected employee.

- The court will also order the employer to pay the full arrears (the underpaid minimum wage difference).

5.2 The Threat of Repeat Offences

- Continuing Offence (Section 46): A daily fine of up to RM1,000 for every day the offence persists after conviction.

- Repeat Offence (Section 47): Penalties escalate to a maximum fine of RM20,000 or imprisonment up to 5 years.

6. Strategic Integration: MWO 2024 and the Progressive Wage Policy (PWP)

The MWO 2024 sets the mandatory legal floor, but the Progressive Wage Policy (PWP) provides the strategic roadmap for growth. This dual-track system encourages productivity-linked salary growth above the minimum wage.

6.1 MWO vs. PWP: Mandatory Floor vs. Voluntary Growth

The MWO is compulsory, aimed at meeting basic needs. The PWP is voluntary, aimed at linking wage growth to skills and productivity. Crucially, full MWO 2024 compliance is a prerequisite for PWP eligibility.

6.2 PWP Incentives: Funding Above the Minimum Wage

The PWP targets local MSMEs and provides government cash incentives (capped at RM200–RM300 per employee monthly) to support wage increments above the RM1,700 minimum wage floor. These incentives are tied to employees completing approved skills training (e.g., 21 hours annually), helping employers offset the wage cascade effect while simultaneously boosting the workforce’s value.

7. Operational Strategy and Final Recommendations

7.1 Mitigating the Wage Cascade Effect

The rise in the minimum wage often causes “wage compression,” forcing employers to raise salaries for mid-level staff to maintain internal pay equity (the wage cascade effect). Strategic participation in the PWP is the most effective way to manage these subsequent wage adjustments with government subsidies.

7.2 Executive Checklist

The PWP targets local MSMEs and provides government cash incentives (capped at RM200–RM300 per employee monthly) to support wage increments above the RM1,700 minimum wage floor. These incentives are tied to employees completing approved skills training (e.g., 21 hours annually), helping employers offset the wage cascade effect while simultaneously boosting the workforce’s value.

- Audit: Immediately identify all employees with a Basic Salary below RM1,700.

- Deadline Adherence: Ensure all necessary adjustments are implemented by February 1, 2025 (Phase 1) and August 1, 2025 (Phase 2).

- Contract Integrity: Verify that commission-based roles guarantee the RM1,700 total minimum wage floor and that all contracts meet the legal definition of basic salary. Eliminate all non-compliant payroll deductions.

- Strategic Shift: Utilize PWP incentives to invest in training and automation, transforming the mandatory minimum wage cost into a productivity advantage.

By treating the MWO 2024 as the non-negotiable legal foundation and the PWP as the pathway to sustained growth, Malaysian businesses can navigate this regulatory change to achieve long-term profitability and compliance.

Conclusion: Navigating MWO 2024 Compliance with

AutoCount Payroll Solutions

The Minimum Wages Order (MWO) 2024 marks a significant change in Malaysia’s wage structure, with the RM1,700 minimum wage becoming mandatory for most employees. Ensuring compliance with this new wage floor, along with accurately calculating EPF, SOCSO, and tax deductions, can be complex and time-consuming for businesses.

Adopting the new RM1,700 minimum wage standard doesn’t have to be complex. With AutoCount Payroll Software, you can automate compliance, avoid costly errors, and keep your workforce records audit-ready.

Disclaimer: This article is provided for general informational purposes only and does not constitute legal or professional advice. While we’ve made every effort to ensure the accuracy of the information at the time of publication, wage laws, regulations and interpretations may change. Employers should consult their own legal or labour-compliance adviser to confirm how the Minimum Wages Order 2024 (MWO 2024) applies in their specific circumstances. Use of our software (AutoCount Payroll Software) does not guarantee compliance, but it may help you automate and monitor key workflows.

Frequently Asked Questions

What is the exact definition of 'wage' under MWO 2024, and can my company include allowances to meet the RM1,700 minimum?

No. The minimum wage under MWO 2024 strictly refers to basic salary (gaji pokok) only. Allowances, commissions, or overtime cannot be included to meet the RM1,700 minimum wage threshold.

When must micro-enterprises (fewer than five employees) start paying the RM1,700 minimum wage?

Micro-enterprises not categorized under MASCO professional activities must comply with the RM1,700 minimum wage starting August 1, 2025.

What are the penalties for failing to pay the RM1,700 minimum wage?

An employer faces a fine of up to RM10,000 for each affected employee for a first offence under Act 732, plus the compulsory payment of all outstanding wage arrears. Repeat offences can lead to imprisonment.

How does the MWO 2024 relate to the voluntary Progressive Wage Policy (PWP)?

The MWO 2024 is the mandatory minimum wage floor. The PWP is a voluntary scheme that provides government cash incentives to employers who increase wages above the RM1,700 minimum wage in exchange for investing in employee training and skills.

Simplify Payroll & MWO 2024 Compliance with AutoCount

Automate statutory calculations, EPF, SOCSO, and MWO 2024 updates — all in one system.