E-Invoice for Donations in Malaysia (2025)

Navigate Malaysia’s new e-Invoicing regulations for donations with ease. Learn about exemptions, implementation timelines, and step-by-step guidance for NGOs, schools, and religious bodies to comply with LHDN’s requirements. Stay compliant and streamline your donation processes today!

Introduction: Navigating the New Digital Donation Landscape

The phased mandatory implementation of e-Invoicing in Malaysia represents a significant shift in how transactions are documented. For entities that rely on donations—such as NGOs, educational institutions, and religious bodies—navigating these new LHDN compliance rules is crucial.

A common misconception is that all donations are exempt. The reality, as clarified by LHDN’s Industry-Specific FAQ on Donations, is more nuanced. While many donations fall outside the scope, approved institutions and specific projects must issue e-Invoices for monetary contributions.

E-Invoice Implementation Timeline

| Implementation Date | Annual Revenue Threshold | Annual Revenue Threshold |

|---|---|---|

| 1 August 2024 | Exceeding RM100 million | Large enterprises |

| 1 January 2025 | RM25 million - RM100 million | Medium-large enterprises |

| 1 July 2025 | RM5 million - RM25 million | Medium enterprises |

| 1 January 2026 | RM1 million - RM5 million | Small enterprises |

| 1 July 2026 | Below RM1 million | Micro enterprises |

Critical Note for MSMEs: Entities with annual turnover below RM500,000 are exempt until their turnover reaches that threshold. However, once mandated, you are mandated forever, even if your turnover later drops below RM500,000.

What is an E-Invoice? A 60-Second Overview

An e-Invoice is not just a PDF receipt. It is a structured digital document (in XML or JSON format) that must be submitted to the Inland Revenue Board (IRBM) for validation through the MyInvois Portal or via an API integration.

The Process: You generate the invoice data, submit it to IRBM, IRBM validates it and returns a unique QR code and reference number, and then you share the validated e-Invoice with your donor.

The Consolidation Concession: For transactions where the buyer (or donor) does not require an e-Invoice, suppliers can issue a single consolidated e-Invoice per month instead of individual ones, simplifying the process for small, recurring donations.

Who is Exempt? When E-Invoices for Donations Are NOT Required

Understanding your exemption status is the first step to compliance. According to LHDN, e-Invoices are NOT required for donations in these two key scenarios:

Purely Religious Institutions

Entities established exclusively for religious worship or the advancement of religion, that have not been approved under specific sections of the Income Tax Act.

Non-Approved Entities:

Any person or organization (including NGOs and schools) that has not been formally approved for tax-deductible donations under sections 44(6), 44(6B), 44(11B), 44(11C), or 44(11D) of the Income Tax Act 1967.

Important Note:

This exemption ceases immediately if your entity is approved under the sections above or manages an approved community project under s.34(6)(h).

E-Invoice Requirement Quick-Reference Table

| Your Entity's Status | E-Invoice Required for Monetary Donations? | Common Examples |

|---|---|---|

| Religious body (purely religious, not s.44 approved) | No | A local mosque, temple, or church without tax approval |

| Any entity not approved under relevant s.44 sections | No | A small, unregistered community charity group |

| Approved institution/fund under s.44(6), (6B), etc. | Yes | Lembaga Zakat, Yayasan PETRONAS, a university foundation |

| Managing an approved project under s.34(6)(h) | Yes | An NGO running an IRBM-approved local development project |

| Conducting commercial activities (any entity) | Yes (for those sales) | A religious body selling books or renting its hall |

When E-Invoices Are Mandatory: 3 Key Compliance Scenarios

Approved Institutions & Funds (S.44 Series)

If your organisation is approved under s.44(6), 44(6B), 44(11B), 44(11C), or 44(11D), you must issue e-Invoices for all monetary donations, regardless of the amount.

Commercial Activities by Any Entity

If your organisation (including religious bodies) engages in non-donation commerce—like selling merchandise, offering paid courses, or renting facilities—e-Invoices are required for those specific sales.

Approved Community Projects (S.34(6)(h))

If you are collecting donations specifically for an IRBM-approved project under this section, you must issue e-Invoices for those contributions.

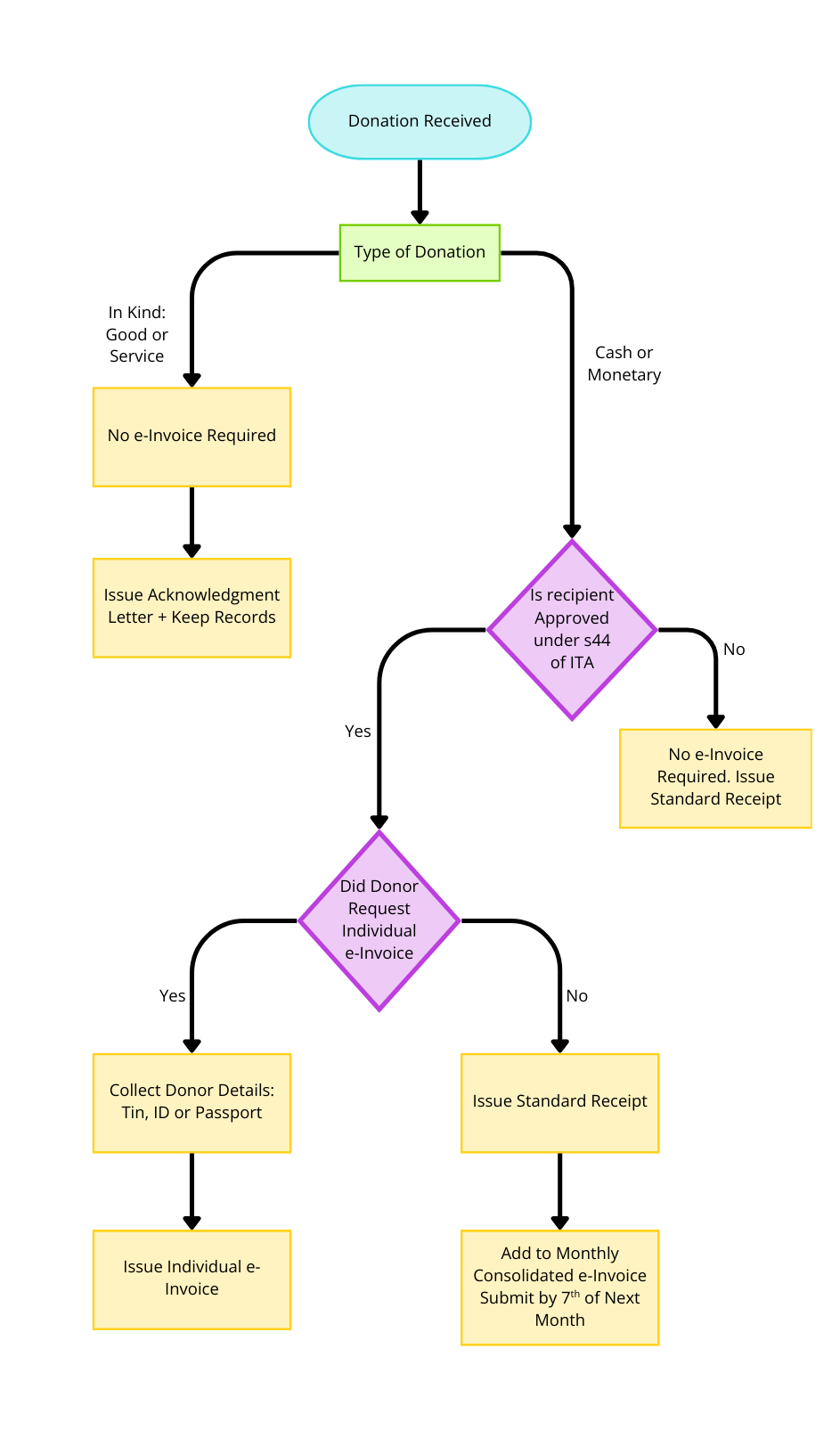

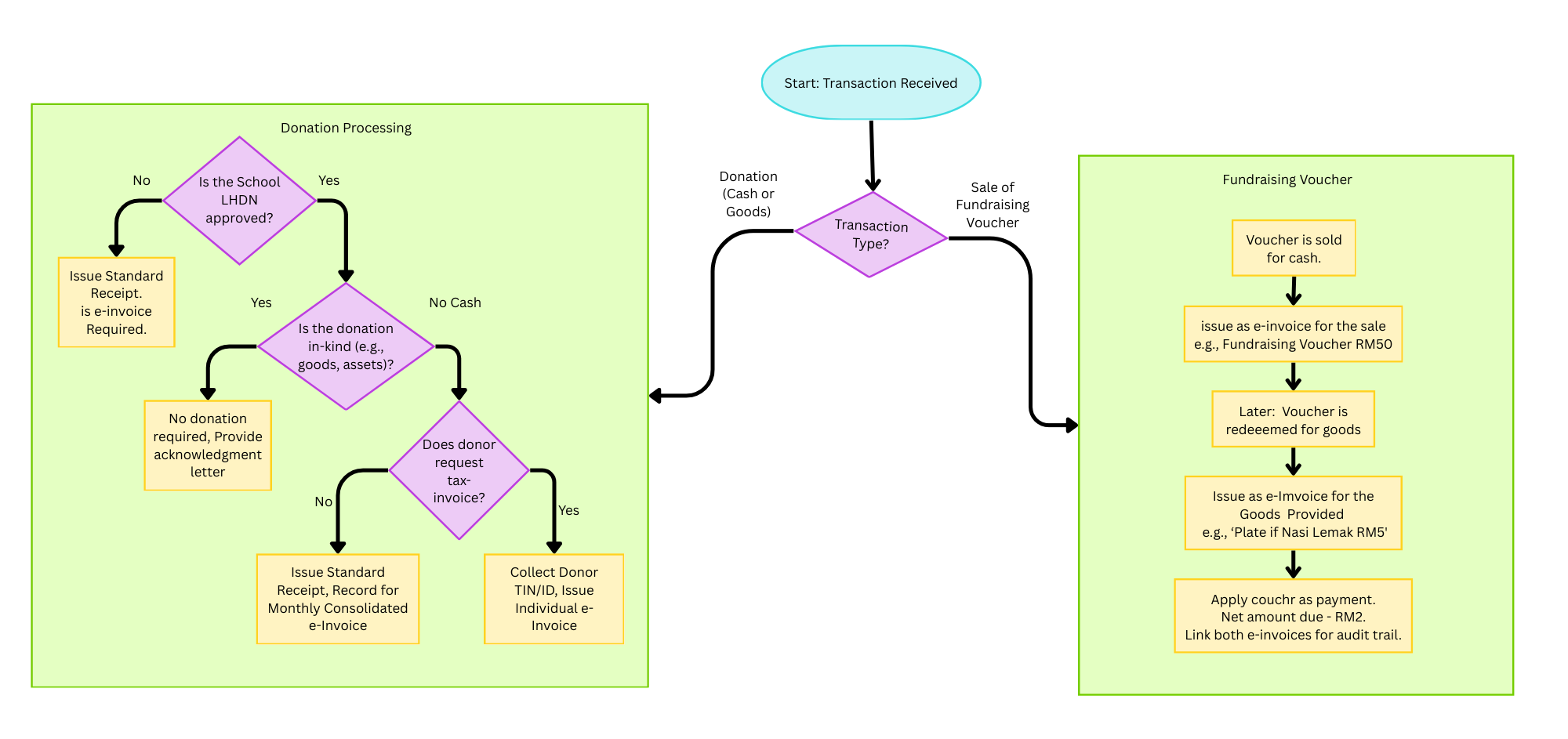

How to Issue E-Invoices for Donations: A Step-by-Step Flowchart

Special Case: In-Kind Donations (Goods & Services)

For non-monetary donations (e.g., computers, equipment, professional services), the recipient organisation is not required to issue an e-Invoice.

Best Practice: Maintain robust internal records, including:

- An acknowledgement letter

- A description and estimated fair value of the goods/services

- The donor's details

- The date of receipt

Practical Situation: E-Invoicing for Schools

Situation 1: Cash Donation to a School

The Situation: A donor gives RM1,000 to a school.

The Compliance:

- If the school is NOT an s.44-approved institution: No e-Invoice needed. Issue a standard receipt.

- If the school IS s.44-approved: Ask the donor if they need an e-Invoice.

If YES, collect their TIN/ID and issue an individual e-Invoice.

If NO, issue a standard receipt and include this donation in your monthly consolidated e-Invoice.

Situation 2: Gift of Computers (In-Kind)

The Situation: A company donates 10 laptops to an NGO.

The Compliance: No e-Invoice is required. The NGO should provide an acknowledgement letter and record the donation in its asset register.

Situation 3: Selling Fundraising Vouchers

The Situation: A school sells RM50 vouchers for its annual fair, redeemable for food and goods.

The Compliance: This is a sale, not a donation.

Upon Sale: You must issue an e-Invoice for the voucher’s full value (RM50).

Upon Redemption: When the voucher is used, issue an e-Invoice for the goods provided and apply the voucher’s value as a credit, making the amount due RM0. Link the two transactions for a clear audit trail.

Practical Examples: E-Invoicing for Schools

Determine Your Status

Check your official LHDN approval letters. Are you approved under s.44 or s.34(6)(h)? This is your most important first step.

Update Donor Collection Processes

Prepare to collect TIN and ID/passport numbers from donors who request an individual e-Invoice. Use the general TIN (EI00000000010) for foreigners without a Malaysian TIN.

Choose Your Issuance Method

For low volume, the free MyInvois Portal is sufficient. For higher volume, consider API integration with your accounting software for automation.

Master the Consolidated E-Invoice

Establish a monthly process to compile all non-requested donations and submit the consolidated e-Invoice by the 7th of the following month.

Train Your Team & Inform Donors

Educate staff on the new procedures. Inform your donors that requesting a tax e-Invoice will require them to provide their details.

Implement Robust Record-Keeping

Store all validated e-Invoices (XML/JSON and PDF) securely for at least 7 years, as required by Malaysian tax law.

Do Donors Need to Issue Self-Billed E-Invoices for Donations in Malaysia?

Donors are not required to issue a self-billed e-invoice for donations in Malaysia. The responsibility to generate e-invoices falls on the recipient organization or institution, particularly for monetary contributions. Donors only need to request an e-invoice if they wish to receive one, and the organization will handle the issuance. This simplifies the process for donors, ensuring they don’t need to manage the technicalities of self-billing, making the donation experience more seamless.

Conclusion: Embrace Compliance to Support Your Mission

The transition to e-invoicing for donations is a manageable process. By first determining your exemption status, you can then implement clear procedures for donor data collection, individual e-invoice issuance, and monthly consolidation.

Leveraging the MyInvois Portal for smaller operations or investing in API integration for larger ones will ensure that your NGO, educational institution, or religious body can continue to focus on its core mission while maintaining full LHDN e-Invoice compliance.

Important Disclaimer:

This guide is for informational purposes based on LHDN guidance as of September 2025. Tax regulations and digital policies are subject to change. Always refer to the latest official documents on the LHDN e-Invoice website and consult with a qualified tax professional or advisor before making compliance decisions for your organization.

Frequently Asked Questions

Are all donations exempt from e-invoicing?

No. Only donations received by purely religious institutions (without s.44 approval) and entities not approved under the relevant s.44 sections are exempt. Approved institutions and projects must issue e-Invoices for monetary donations.

Our religious body is tax-exempt but not s.44-approved. Do we need e-invoices?

No. Your exemption from e-invoicing for donations remains. You only need to issue e-invoices for commercial activities (e.g., rental income, sales of goods).

What if a donor is a foreigner without a Malaysian TIN?

Use the special General TIN: EI00000000010 and provide the donor’s passport number in the required field

Are in-kind donations like equipment subject to e-invoice?

No. The recipient does not issue an e-invoice for gifts of goods or services. Maintain detailed internal records and acknowledgement letters.

Learn E-Invoicing with Our Expert-Led Classes

Ready to master e-invoicing and streamline your business? Join our comprehensive class and get hands-on guidance!