EPF (Employees Provident Fund) Training Manual (2025 Update)

A complete 2025 EPF training guide for Malaysian payroll teams. Learn contribution rules, calculation methods, and compliance updates under the latest EPF Act amendments.

The Employees Provident Fund (EPF), or KWSP (Kumpulan Wang Simpanan Pekerja), is the official statutory body managing compulsory retirement savings for all private sector employees in Malaysia. As a payroll professional, your primary responsibility is ensuring strict adherence to the EPF Act 1991 for accurate monthly EPF contributions.

Provides mandatory pre-calculated contribution amounts (up to RM20,000).

Second Schedule

Detailed exemptions list.

Identifies employees excluded from mandatory contributions.

2. Eligibility and Registration

2.1 Mandatory EPF Contributors

Contributor Type

Eligibility Criteria

Key Compliance Action

Employees

Malaysian Citizens / Permanent Residents (PR) aged 18–75. Foreign Workers with valid passes (mandatory from Oct 2025).

Must obtain an EPF membership number via Form KWSP 3.

Employers

Any entity employing one or more eligible individuals under a Contract of Service.

Must register with EPF within 7 days of the first hire.

2.2 EPF Registration Procedures

New Employer Registration: Submit Form KWSP 1 and necessary business registration documents. Registration is highly encouraged via thei-Akaun (Employer) portal.

Employee Records: Ensure employee demographic and salary data is accurately registered to prevent errors (CTML - Contribution Without Complete Information).

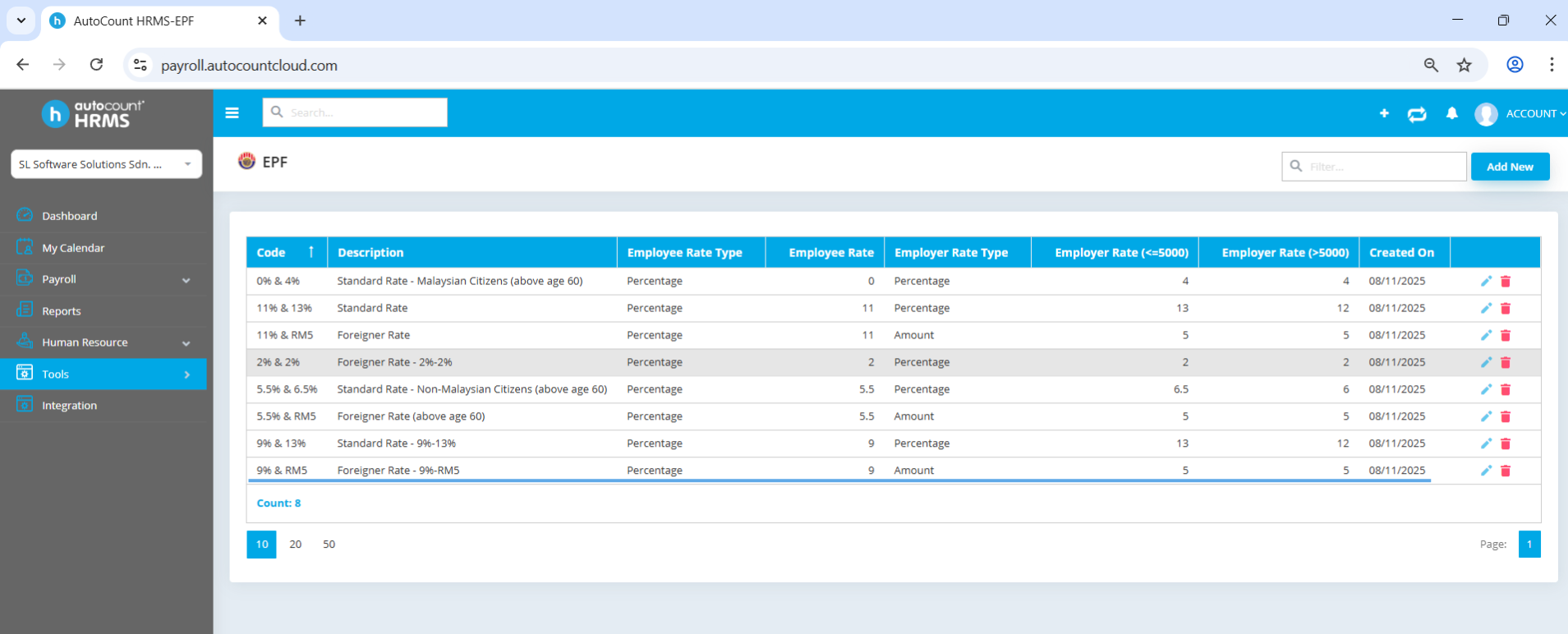

3. EPF Contribution Rates (2025 Third Schedule)

3.1 Statutory Contribution Rate Matrix (Effective Oct 2025)

Rates are determined by the Third Schedule, based on the employee’s status and EPF Contributable Wage (ECW) bracket.

Category

Age Group

Monthly Wage (ECW)

Employer Rate

Employee Rate

Third Schedule Ref.

Malaysian / PR

Below 60

≤ RM5,000

13%

11%

Part A

Malaysian / PR

Below 60

> RM5,000

12%

11%

Part A

Malaysian

60–75

Any amount

4%

0%

Part E

Permanent Resident

60–75

≤ RM5,000

6.5%

5.5%

Part C

Non-Malaysian

Any age

Any amount

2%

2%

Part F

3.2 Rate Application Rules

Age Change Rule: The new rate (e.g., transition to age 60-75) applies for the entire payroll month in which the employee's birthday falls.

Voluntary Contribution (VE): Employees can increase their deduction via Form KWSP 17A. Employers must process this change through i-Akaun.

For more detailed information on mandatory employer contributions to the Employees Provident Fund (EPF), including applicable rates and responsibilities, employers can refer to the official Employer Contribution to Employees page on the EPF website.

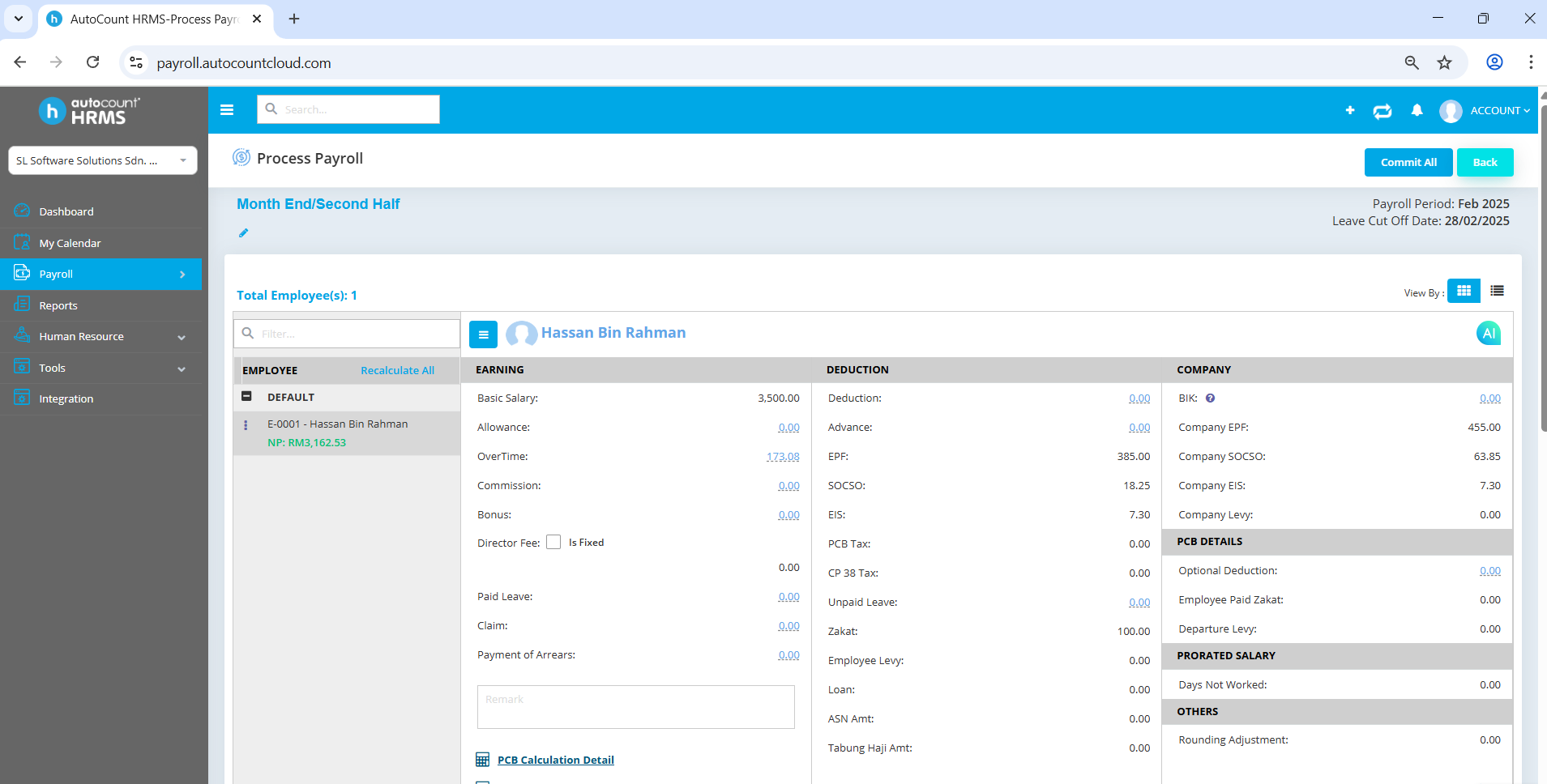

4. EPF Calculation Methodology

4.1 Defining EPF Contributable Wage (ECW)

Definition of "Wage" under Employees Provident Fund Act 1951

“Wages” means all remuneration in money, due to an employee under his contract of service or apprenticeship whether agreed to be paid monthly, weekly, daily or otherwise and includes any bonus, commission or allowance payable by the employer to the employee whether such bonus, commission or allowance is payable under his contract of service, apprenticeship or otherwise, but does not include:

service charge

overtime payment

gratuity

retirement benefit

retrenchment, lay-off or termination benefits

any travelling allowance or the value of any travelling concession; or

any other remuneration or payment as may be exempted by the Minister

Meeting the 15th of the month deadline is the most critical EPF compliance point.

Date Range

Key Action

Compliance Mandate

1st - 10th

Finalize the payroll data and confirm the EPF Payable Amount for all employees.

Accurate Calculation

10th - 14th

Final submission file generation (e-Caruman CSV).

Verification

15th

REMITTANCE DEADLINE. Submit Form A and pay the total EPF Payable Amount electronically.

Statutory Deadline (KWSP)

For a deeper understanding of Malaysia’s statutory payroll reporting process, which covers monthly submissions, statutory forms and compliance tracking, visit our Statutory Payroll Reporting in Malaysia Guide

6.2 Digital Submission via i-Akaun

i-Akaun (Employer) is the official platform for: file submission (Form A), payment via e-Caruman/FPX, and managing employee records (KWSP 3, 8D, etc.).

Audit Trail: Retain all digital receipts and monthly contribution statements for 7 years.

7. Penalties and Enforcement

7.1 Non-Compliance Penalties

Failing to adhere to the EPF Act 1991 can result in severe legal consequences for the employer and directors.

Late Payment Charge: Compound interest calculated at 1% per month on the overdue amount.

Legal Action: Fines of up to RM10,000 per employee or imprisonment up to three years for willful non-payment or fraudulent statements.

Dividend Liability: The employer must pay the employee any lost dividends due to late contribution remittance.

This key legislative change mandates EPF contribution for all non-Malaysian citizens (excluding domestic workers) holding valid employment passes, effective from the October 2025 wage.

Phase

Action Item

System Update

Incorporate Part F (2% + 2%) logic into payroll software and verify foreign worker categorization.

Registration

Ensure all non-member foreign employees are registered with EPF before the October payroll run.

Remittance

Submit the first mandatory contribution for these employees by November 15, 2025.

9. Payroll Resources & Guides

Explore our comprehensive guides to understand statutory requirements and streamline your payroll processes in Malaysia.

Manage your payroll easily with AutoCount Payroll, a system built for accuracy and compliance with Malaysia’s EPF and statutory rules. It automates salary calculations, EPF contributions, and reports -saving you time and reducing errors.

Disclaimer

The information provided on this page is for general guidance only and does not constitute professional advice. While we strive to keep the content accurate and up-to-date, the laws and regulations of the Employees Provident Fund Organisation (EPF) in Malaysia may change, and individual circumstances may vary. You should not rely solely on the information here when making decisions related to EPF training, contributions, withdrawals, compliance or any other official matter. For specific advice tailored to your situation, please consult a qualified professional or contact EPF directly. We disclaim any liability for losses or damage arising from relying on this content.

Is Your EPF Contribution in Malaysia Fully Compliant?

Stay ahead with AutoCount: automate EPF calculations, monitor contributions, and ensure compliance for 2025.